2024 Oil & Gas Emissions Cap POLICY TOOLKIT – 5a. The 2030 Cap Level Is Not Ambitious Enough – The Numbers

Oil & Gas Cap Policy Toolkit

5. The Problems With The Framework

Toolkit Contents

- EXECUTIVE SUMMARY

- BACKGROUND – THE OIL & GAS SECTOR GHG EMISSIONS PROBLEM

- BACKGROUND – A TRICKY JURISDICTIONAL BALANCE

- HOW THE O&G EMISSIONS CAP WORKS

- THE PROBLEMS WITH THE FRAMEWORK

- The 2030 Cap Level Is Not Ambitious Enough – The Numbers

- The Cap Proposed by the Framework Will Make It Almost Impossible to Meet Our Canada-Wide 2030 Target

- The Framework’s O&G Emissions Cap Will Do Less Work Than It Appears

- The O&G Emissions Cap Has Effectively Been Dictated by the Oil and Gas Producers

- The Oil and Gas Industry’s Re-investments to Reduce Emissions Has Been Contemptible

- The O&G Emissions Cap is based on O&G Production Increasing by 2030

- The “Other Compliance Units” Are Mostly a Very Bad Idea

- COMPLIANCE FLEXIBILITIES

- SUGGESTED RESPONSES TO THE FRAMEWORK’S DISCUSSION QUESTIONS

- I DON’T HAVE TIME TO READ THIS LONG DOCUMENT. WHAT SUBMISSIONS SHOULD I CONSIDER MAKING?

- ACRONYMS & GLOSSARY

The fundamental problem with the Framework is that it simply lets too large a quantity of GHGs be emitted from oil and gas production each year.

There are three main components of the problem. The first is that the proposed “emissions cap level” and the “legal upper bound” for emissions are too high. This is discussed in detail below.

The second is that the Framework proposes several “compliance flexibilities”. They serve to let O&G producers emit more and also create the false impression that the O&G Emissions Cap is achieving much more than it really is. The compliance flexibilities also have vulnerabilities that, if not managed carefully, could result in more GHGs being emitted than the legal upper bound. Each compliance flexibility is examined in section 6.0.

Third, Canadians might be surprised to see that the O&G Emissions Cap is based on O&G production increasing between now and 2030. See section 5.6 for more information.

a. The 2030 Cap Level is Not Ambitious Enough – The Numbers

An understanding of the numbers is essential to understanding the proposed Framework.

The 2030 Emissions Reduction Plan: Canada’s Next Steps for Clean Air and a Strong Economy (the “ERP”), published by ECCC on 29 March 2022, set out in considerable detail the programs and policies that ECCC would implement to reach our pledge under the Paris Agreement of reducing Canada’s GHG emissions by 40 to 45% below 2005 levels by 2030. [36]

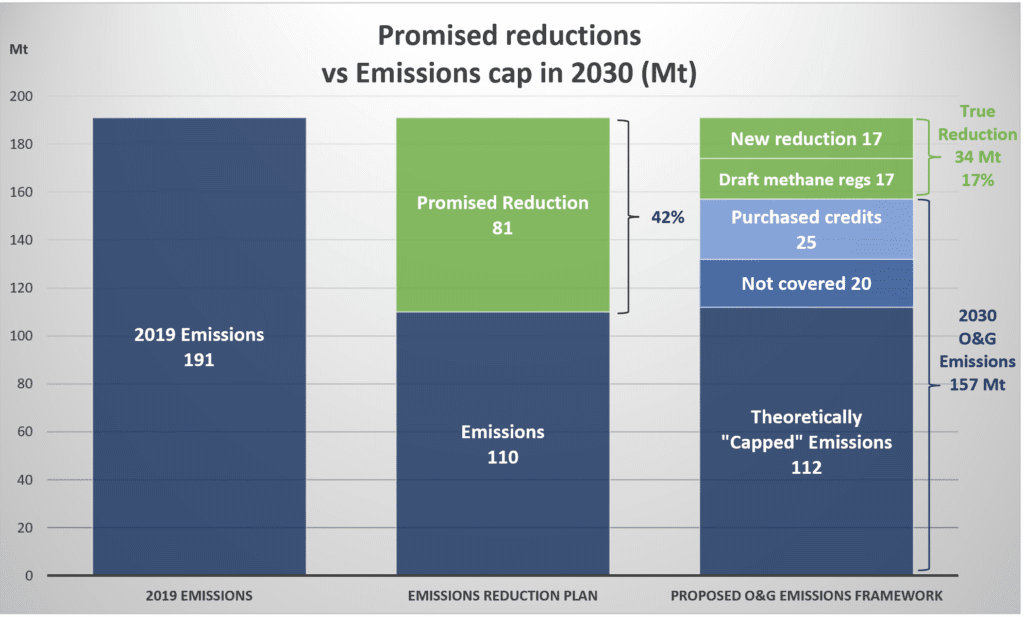

The ERP called for reductions in GHG emissions from oil and gas production of 31% from 2005 levels by 2030. Because emissions from oil and gas production had risen considerably between 2005 and 2019, this equated to reductions of 42.5% from 2019 levels by 2030. [37]

However, instead of cuts of 42.5% from 2019 levels, the Framework proposes cuts of only 17.8%.

Canadians expect the federal government to keep its promise on climate change and not just follow the demands and wishes of the oil and gas industry. All Canadians who care about the climate and a livable future for all should use the public consultation to ensure that ECCC knows this.

To do so, we must arm ourselves with the facts and knowledge of how this situation has come to be.

In the ERP, ECCC included a long table that considered various GHG emitting sectors. For the “Oil and Gas” sector, it provided the following data: [38]

Figure 1: Canadian Oil and Gas Sector Actual and Projected GHG Emissions

Sector | Where we were in 2005 (Mt) | Where we were in 2019 (Mt) | Where we could be in 2030 (Mt) | Per Cent Reduction from 2005 Levels |

| Oil and gas | 160 | 191 | 110 | -31% |

According to the ERP on 29 March 2022, therefore, the O&G Emissions Cap needed to cut 81 Mt of emissions from 2019 levels by 2030:

191

-110

81

The first thing that ECCC is proposing to that makes the O&G Emissions Cap more lenient is to simply remove 20 Mt of emissions, which are those from downstream oil refineries and gas transmission pipelines, from the scope of the emissions that need to be reduced.

On 18 July 2022, ECCC published Options to Cap and Cut Oil and Gas Sector Greenhouse Gas Emissions to Achieve 2030 Goals and Net-Zero by 2050 Discussion Document (the “Discussion Document”). [39]

The Discussion Document stated “In addition to upstream activities, the government is seeking input on whether the cap should apply to natural gas transmission pipelines and petroleum refineries.” [40] Of the 22 Questions it posed, Question #8 was “Should the cap include petroleum refineries and natural gas transmission pipelines?” [41]

Under the heading “Scope of application”, the Framework states: “The emissions cap-and-trade system would apply to LNG facilities and to upstream oil and gas facilities, including offshore facilities.” [42] Petroleum refineries and natural gas transmission pipelines have now been omitted.

In 2019, emissions from (downstream) petroleum refining were 19 Mt and emissions from natural gas distribution were 1.1 Mt (which we shall round down to 1 Mt). [43]

As such, ECCC has made the goal easier, and the required reductions smaller, simply by taking those 20 Mts out of consideration:

191

- 20

171

Under the heading “Emission allowances and legal upper bound on emissions in 2030”, the Framework states:

There are two key values in the proposed approach: (1) the emissions cap level, which is equivalent to the total emission allowances issued by the government for a given year, and (2) the legal upper bound, which is the maximum emissions the sector will be allowed to emit that year, comprised of the total number of emission allowances issued plus the maximum allowable quantity of other eligible compliance units. [44]

The Framework proposes that the 2030 emissions cap (the number of allowances issued) be set at between 106 Mt and 112 Mt CO2e. It proposes that the legal upper bound in 2030 of between 131 Mt and 137 Mt. [45]

From the 171 Mts of emissions still covered by the scope of the O&G Emissions Cap, therefore, we can remove the 2030 “emissions cap level” of 112 Mts:

171 Mt

- 112 Mt (“emissions cap level”, i.e. emissions permitted by allowances)

59 Mt

The Framework proposes that oil and gas producing companies can emit an annual total of 25 Mt of “other compliance units” in 2030. [46]

Regarding those “other compliance units”, the Framework states:

It is proposed that… facilities have the option to remit domestic offset credits or make contributions to a decarbonization funding program to cover a limited portion of their GHG emissions. Consideration is also being given to allowing facilities to remit compliance units that represent mitigation outcomes that have been authorized for use by Canada as internationally transferred mitigation outcomes (ITMOs) to cover a portion of their GHG emissions. [47]

59 Mt

- 25 Mt (“other compliance units”, i.e. offset credits or emissions reduction fund)

34 Mt

And that’s how we get from 81 Mt of emissions reductions from O&G production called for in the ERP to only 34 Mt proposed by the Framework.

Returning to the 2019 emissions of 191 Mt set out, as above, in the ERP, we can see this:

34 / 191 x 100 = 17.8%

So, again, instead of the 42.5% of emissions reductions from 2019 levels called for by the ERP, ECCC is now proposing less than half of that: 17.8%.

You can reach the same conclusion by starting at the other end:

Start with the 112 Mt “emissions cap level”, i.e. the emissions permitted by allowances.

Add in the 25 Mt of additional emissions permitted by “other compliance units”.

112 Mts

+25 Mts

137 Mts

Then add in the in the 20 Mts that is permitted from downstream refining and gas pipelines, because the Framework will now simply not apply to them:

137 Mts

+ 20 Mts

157 Mts

Those 157 Mts of emissions are 47 Mt, or 42.7% over the ERP’s “Where we could be in 2030” of 110 Mts.

This table shows 2019 emissions from O&G Production, the reduction to those emissions called for in the ERP, and what the proposed Framework would actually accomplish.

Do not be fooled when the Framework states that ECCC’s proposal will result in emissions reductions that “would be 35% to 38% below 2019 emission levels”. [48] That is because they have made the goal easier by removing the 20 Mt from downstream oil refineries and emissions from gas pipelines from the scope of emissions covered and because they are counting the 25 Mt of “compliance flexibilities” (from carbon offset credits and payments into a “decarbonization fund”) as emissions reductions.

Saying the same thing another way, ECCC is not counting the 25 Mt of additional emissions that will be permitted from “compliance flexibilities”. ECCC is effectively saying that, since this 25 Mt of emissions from the O&G sector will be “offset” by emissions reductions elsewhere, the only emissions coming from oil and gas production is the 112 Mt. However, as will be discussed in section 6.0 below, those emissions reductions are far from certain.

Recommendations:

Tell the federal government (using references to the papers we cite here, as you may wish):

• The proposed level of the oil and gas sector emissions cap is nowhere near ambitious enough. It is not aligned with the emissions reductions being required in other sectors of the economy, with Canada’s 2030 Target under the Paris Agreement (enshrined in law in the Canadian Net-Zero Emissions Accountability Act), or with a pathway that sees Canada reaching net-zero GHG emissions by 2050.

• Hold the federal government accountable to deliver the emissions reductions promised in their 2022 Emissions Reduction Plan, which suggested the cap for the O&G sector would be 110 Mt in 2030. [49] That means:

• The “compliance flexibility” allowing fossil fuel companies to pay to emit 25 Mt per year over and above the cap must be eliminated. Another way to put it is that the legal upper bound for emissions should be the same amount as the emissions cap.

• The legal upper bound for oil and gas sector emissions in 2030 should be no more than the 110 Mt promised in the Emissions Reduction Plan.

• The scope of application of the cap on oil and gas sector emissions should be the same as envisioned in the Emissions Reduction Plan. Downstream pipelines and refineries were to be included, but have been omitted from the cap proposed in the Framework. They must be put back in scope.

• Despite the jurisdictional challenges discussed above, the federal government should not be excessively timid. The Oil & Gas Emissions Cap level should be considerably more stringent.

Citations

- Environment and Climate Change Canada. 2030 Emissions Reduction Plan: Canada’s Next Steps for Clean Air and a Strong Economy. Released 29 March 2022. Retrieved on 14 August 2022 from https://publications.gc.ca/site/eng/9.909338/publication.html

- Percentages obtained by the number on ERP, pp. 89-90.

- ERP, pp. 89-90.

- Environment and Climate Change Canada (ECCC), Options to Cap and Cut Oil and Gas Sector Greenhouse Gas Emissions to Achieve 2030 Goals and Net-Zero by 2050 Discussion Document, 18 July 2022. (Hereinafter the “Discussion Document”). Retrieved on 15 December 2023 from https://www.canada.ca/en/services/environment/weather/climatechange/climate-plan/oil-gas-emissions-cap/options-discussion-paper.html

- Discussion Document, p. 17.

- Discussion Document, p. 29.

- Environment and Climate Change Canada (ECCC), A Regulatory Framework – To Cap Oil and Gas Sector Greenhouse Gas Emissions, 7 December 2023, p. 2.

- Environment and Climate Change Canada (ECCC), National Inventory Report – 1990-2019: Greenhouse Gas Sources and Sinks in Canada – Canada’s Submission to the United Nations Framework Convention on Climate Change, Part 1, p. 57, Table 2-12.

- Framework, p. 4.

- Framework, p. 5.

- Framework, p. 5.

- Framework, p. 7.

- Framework, p. 5.

- Environment and Climate Change Canada. 2030 Emissions Reduction Plan: Canada’s Next Steps for Clean Air and a Strong Economy. Released 29 March 2022. Retrieved on 14 August 2022 from https://publications.gc.ca/site/eng/9.909338/publication.html